FICO UK Credit Card Market Report: December 2023

High prices lead to highest average credit card spend and balances since FICO records began

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20240222259009/en/

The latest FICO

Highlights

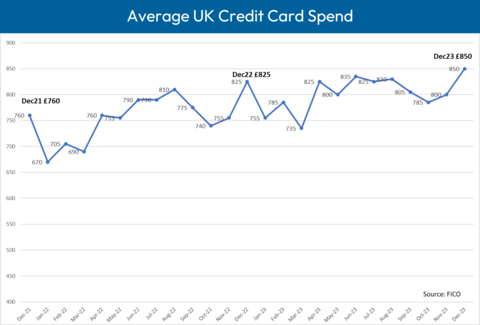

- Average spend increased by 5.9% on the previous month, to £850

- Average balances rose by 2.2% month-on-month and 7.2% year-on-year, leading to an average balance of £1,780

- 14.8% more customers missed a credit card payment month-on-month and 0.5% more compared to the same month in 2022

- There has been a 1.3% decrease in the average balance for those customers missing one payment

Key Trend Indicators –

|

Metric |

Amount |

Month-on-Month

|

Year-on-Year

|

|

Average |

£850 |

+5.9% |

+2.9% |

|

Average Card Balance |

£1,780 |

+2.2% |

+7.2% |

|

Percentage of Payments to Balance |

36.6% |

-0.2% |

-4.9% |

|

Accounts with One Missed Payment |

1.7% |

+14.8% |

+0.5% |

|

Accounts with Two Missed Payments |

0.3% |

+0.9% |

+1.9% |

|

Accounts with Three Missed Payments |

0.7% |

+7.7% |

+5% |

|

Average Credit Limit |

£5,615 |

+0.1% |

+0.8% |

|

Average Overlimit Spend |

£90 |

0% |

-4.4% |

|

Cash Sales / Total Sales |

0.8% |

-10.2% |

+0.7% |

Source: FICO

FICO Comment

Increases in spend always occur in December, and 2023 was no exception with a 5.9% month-on-month rise, taking the average spend to £850. This is the highest spend since FICO records began in 2006.

The average balance continued to trend upwards, as expected in the lead up to Christmas.

Another pattern typical of December was the amount paid off credit card balances as shoppers focussed their cashflow on Christmas spending. In

Pre-COVID, the average payment compared to the overall balance was approximately 30%, but with lockdown and increased savings this rose to 42%. The FICO data now shows this dropping back, although it is currently still 6% higher than before the pandemic.

Another sign of pressure on finances was the number of customers missing one, two and three payments. This increased from November to

Issuers should note that established customers – those who have had their credit card between one and five years – are the most likely to miss payments. This group contains customers whose 0% offers have expired, and they are now paying off balances at the standard rate. FICO recommends monitoring this group for signs of vulnerability and indebtedness. Now is a great time to review existing collections strategies and examine whether anything more can be done to proactively identify and assist financially distressed customers.

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80% of

About FICO

FICO (NYSE: FICO) powers decisions that help people and businesses around the world prosper. Founded in 1956, the company is a pioneer in the use of predictive analytics and data science to improve operational decisions. FICO holds more than 200 US and foreign patents on technologies that increase profitability, customer satisfaction and growth for businesses in financial services, insurance, telecommunications, health care, retail and many other industries. Using FICO solutions, businesses in more than 100 countries do everything from protecting 2.6 billion payment cards from fraud, to improving financial inclusion, to increasing supply chain resiliency. The FICO® Score, used by 90% of top US lenders, is the standard measure of consumer credit risk in the US and other countries, improving risk management, credit access and transparency. Learn more at www.fico.com.

FICO and TRIAD are registered trademarks of

View source version on businesswire.com: https://www.businesswire.com/news/home/20240222259009/en/

For further comment on the FICO

FICO

ficoteam@harrisonsadler.com

0208 977 9132

Source: FICO